Marco Fava, Managing Director, CleverAdvice

On 15 November 2020 Nexi Payments, Italy’s leading payment services providers, and Nets, a leading provider of payments solutions operating in the Nordics and throughout central and eastern Europe, signed a binding framework agreement with the aim of merging the two groups through an all-share exchange.

That’s just a few weeks after Nexi announced a merger agreement with SIA, Italy’s leading payment processor and network services provider.

They appear to be counter-market responses to the merger between Worldline and Ingenico, announced in early February 2020, and expected to be operatively effective by January 2021. Both mergers strongly push the consolidation in the payment industry underway in Europe and globally, no doubt about it.

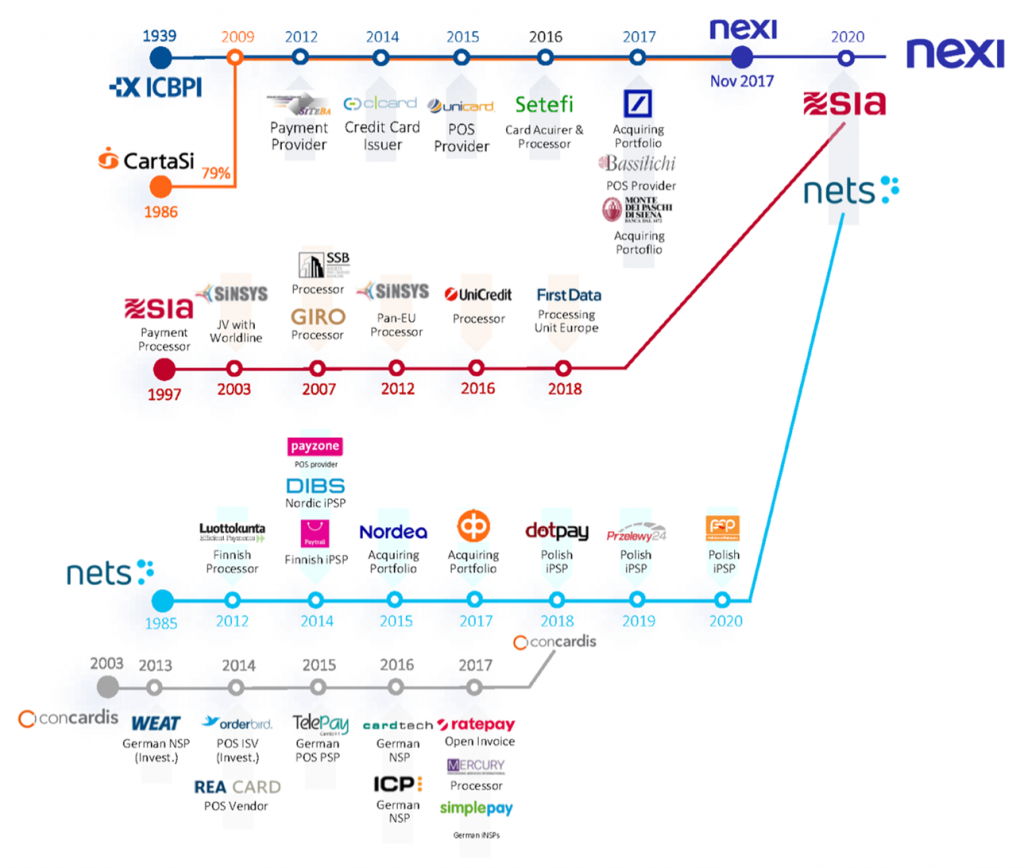

The Nexi–SIA merger

Nexi Payments offers issuing and acceptance services and solutions – in-store, online and mobile – digital payments and loyalty solutions – banking services through a full banking license – including clearing and settlement, instant payments and ATM management solutions – and open banking services to banks, payments and electronic money institutions and government agencies and it is among the 23 ACHs members of the European Automated Clearing House Association. Nexi offers payment services and solutions only in the Italian market where it retains a strong leading position: over 150 banks served, nearly 60% market share in card issuing and digital payments and over 70% share in merchant services and solutions. The significant share of on-us transactions translates into strong margins and offers potential to develop a more streamlined SCA-authorisation procedure, aimed at improving conversion rates.

In the last 5-7 years the Italian payments market has been growing at 10% per year with ecommerce twice as fast. Nevertheless, significant potential lays ahead: Italians hold a number of e-payments instruments in line with the average European, but cash is still king for many, particularly outside the main cities. The use of cash is prone to the shadow economy and helps organised crime, issues the government is keen in fighting with an initiative aimed at strongly push e-payment usage. Consumers will receive a 10% cashback on all in-store e-payment transactions up to EUR 1500 per semester from 1 January 2021 until 30 June 2022 and a trial period in December 2020. Nexi is naturally positioned to strongly benefit from a boost in e-payment transactions with a government blessing.

SIA, on the other hand, is a leading payment processor and interbank network provider, a developer of payment solutions and platforms – including STEP2 and RTGS at the European level – and capital market network infrastructures. SIA developed TARGET2 to link the central banks in the Eurosystem with major European banking groups and deployed a number of innovative payment solutions for leading transit systems operators. SIA is headquartered in Italy, but it’s scope is international as it is leading European projects since the late 1990s and since the last decade is serving clients as far as Canada and New Zealand, where it competes with peers including ACI Worldwide, Fiserv, Vocalink, FIS, FirstData, and Pymentus.

The main rationale behind the merger is offer complementary, aimed at creating a player with broad capabilities to cover the entire payments value chain. A second rationale is to build critical mass under one roof to better compete in an ecosystem where size is increasingly important due to the consolidation trend in place. Some in the industry mentioned a further rational: the recent Italian government’s push to stimulate the use electronic payments. I believe this is just a perception as the Nexi-SIA merge is unlikely to have a significant effect on the end user.

Adding Nets to Nexi-SIA

62% of Nets revenue is generated from merchant services – including ecommerce solutions – the rest being issuing and eSecurity solutions. Customer reach is pan-European with leadership in the advanced Nordics markets and strong presence in central and eastern Europe.

Offerings of Nexi-SIA and Nets mix similarities and differences, but no overlap in geographical reach. Here the rationales behind the merger are to exploit growth potentials of attractive but still underpenetrated European markets through a full range of payment solutions across the value chain, and create value from leveraging synergies of both propositions and scale.

The new group will be the leading European acquirer servicing 2.4 million merchants and the payment provider with the highest EBITDA (EUR 1.5 billion) – including EUR 300 million in estimated recurring synergies – on revenue of EUR 2.9 billion in 2020.

The all-share nature of the transaction suggests shareholders’ confidence in Nexi’s management – whom will manage the new group – and in its strong profitability, which positions it well for further growth through acquisitions as availability of capital should not be an issue.

Nexi will also reduce its revenue concentration as today the top 10 clients account for 48% of Nexi’s revenue. By merging with Nets, the share of the top-10 clients’ revenue will be reduced to 27%, lowering market risk.

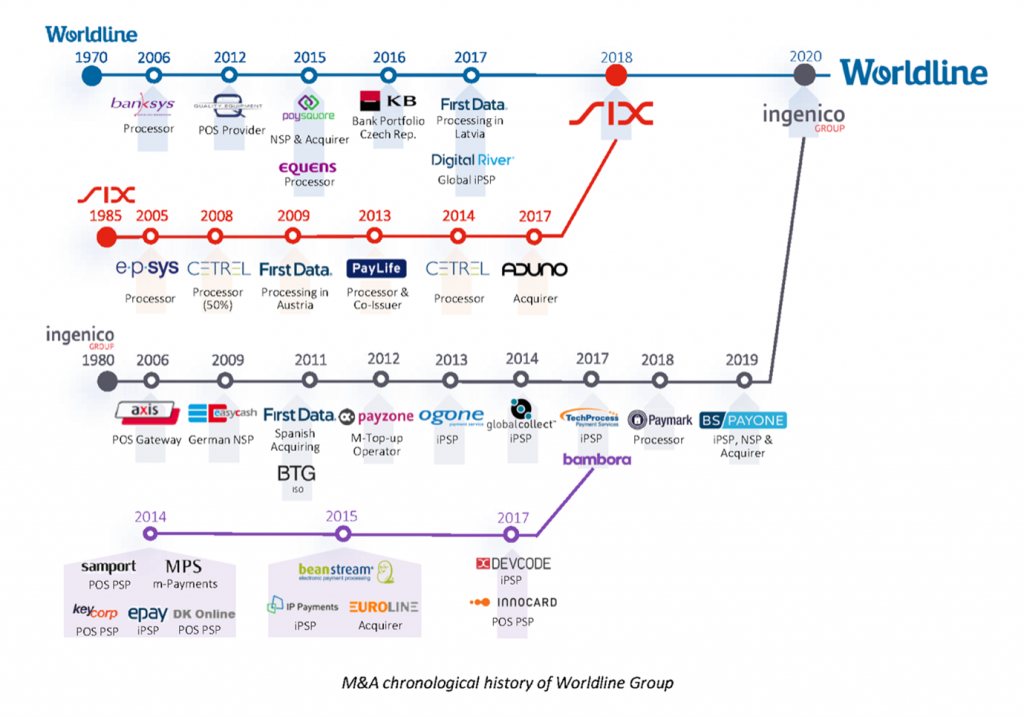

The Worldline–Ingenico merger

Worldline is the leading payment services provider in Europe with 2019 revenue of EUR 2.4 billion. It covers the entire payment value chain through three main business lines: 1. Merchant Services – in-store, online and mobile acceptance solutions, data analytics, loyalty, and private label card services; 2. Financial Services, that allow banks to outsource payment cards issuance and payments authorisation, digital payment transactions processing and multi-platform online banking services; 3. Mobility and e-Transactional Services including e-government collection services, e-ticketing and payments solutions for mobility services (transit systems, trains, parking, car and bike sharing).

Ingenico is the world leading payments terminal manufacturer – with 37% market share and 30 million+ terminals operating worldwide – and a European merchant services business with strong online offering. The partnership with the German savings banks and the PAYONE joint venture have given Ingenico the leadership in the German commercial acquiring market.

The deal will create the world’s 4th largest payment services provider, with expected 2020 revenue of EUR 5.5 billion (net of interchange fees), EUR 1.1 billion in EBITDA and 1 million merchants served.

With respect to the broader payments market, the two mergers trigger considerations and insights in particular related to upsides, downsides and challenges.

Upsides

The presence of two large European payments groups is likely to enhance efficiency and customers may benefits from more cost-effective services and solutions, in particular in the regions where each group is keen to expand and face fiercer competition.

It is good news for Europe as a whole as it should curbs the potential market-entry of the larger US conglomerates Fiserv and Fidelity National Information Services and limit the expansion of Global Payments.

Downsides

In the long run consolidation may stimulate focusing on operational efficiency – to please investors – more than innovation. For instance, despite defining themselves Paytechs (Nexi and Nets) and leading payment innovator (Worldline), so far both groups have relied on integrating open banking services outsourced from fintech companies as opposed to develop their own. This may be good for a few fintechs, but the presence of two behemoths may limit opportunities of many others as in practical terms it may become necessary to deliver their innovative services through one of the two conglomerates with few alternatives.

Challenges

We expect a limited challenge in effectively integrate the companies within the two groups due to limited overlapping in services offered and/or geographical reach.

Competing effectively in a few attractive and unpenetrated markets – e.g. Germany – is likely to be a challenge, more so in the profitable merchant services space, due to fierce competition. Growing through local acquisitions in some instances may prove to be the way to go.

On the issuing side it would be important to fully understand the needs and preferences of a diversified European customer base and offer tailored solutions in specific markets, possibly through local partnerships.

We expect Worldline to be able to better compete in the US market due to its size, getting closer to that of its US peers, although competing in the USA will remain a significant challenge.

Nexi is likely to invest in developing cross-border acquiring and marketplace propositions to be able to offer both a wider value-added services range to large and smaller merchants and expand in southern Europe.

The Nexi-SIA-Nets group may limit investments in SIA network-related services which would not favor a smooth integration and potentially trigger a spin-off of specific activities.

About CleverAdvice:

CleverAdvice is an independent professional services firm focused on the payments industry and active member of the European Payments Consulting Association (EPCA). Areas of expertise include Open Banking strategies and use cases, Digital onboarding, Customer journey, Strong Customer Authentication, Commercial cards and payments, Instant payments, Conversion at checkout, and Customer retention techniques.

www.cleveradvice.eu